Material Uncertainty

"Where the degree of uncertainty in a valuation falls outside of parameters that might normally be reasonable and accepted" - VPGA 10, RICS Red Book

What is material uncertainty?

Valuation Reports and documentation are a critical and defining feature of the Red Book Global Standards process.

A valuation report must clearly and accurately set out the conclusions of the valuation in a manner that is neither ambiguous nor misleading and does not create a false impression.

In times of uncertainty, that would not be reasonable, and the valuer must draw attention and comment on this uncertainty.

Why is it needed?

There are a several situations where a Material Uncertainty clause is required. We have noted a few of these below.

- Lack of Comparable Data - When certain unknown events happen and cause the market to freeze, there is often a lack of immediate comparable data and the clause highlights that the valuation may be based on limited data.

- Transparency in Exceptional Times - The clause highlights that the valuation is prepared in exceptional circumstances where there is not the same degree of certainty.

How we mitigate?

The Real Estate X team worked through the Covid 19 pandemic and helped Clients navigate and make sense of valuation impact. We can use the experience gained during that time and apply it to the advice we continue to give to Banks, financial institutions and stakeholders across the Emirates.

In exceptional times, market experience is of paramount importance.

Current Situation

UAE Hospitality 7-Day Demand

UAE Hospitality 7-Day Revenue

Forward Booking

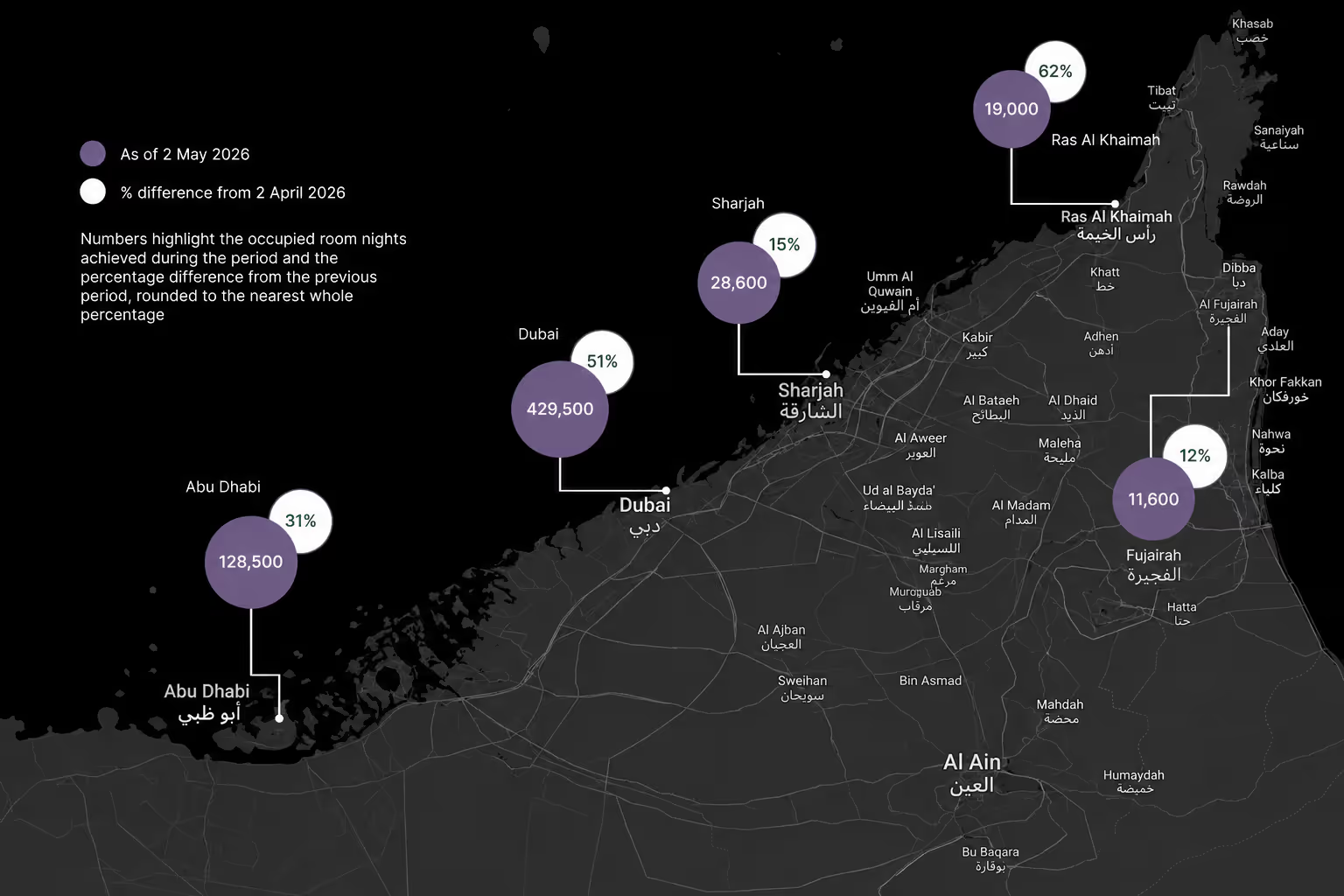

Critical to assessing demand levels is forward booking, it plays a key role in helping a valuer understand the current sentiment and likely occupancies going forward.

As of mid-April 2026, both Abu Dhabi and Dubai had a current 90 day forward booking at 14%, vs the same period during 2025 of 34%.

Pickup, or the proportional difference between rooms booked during the previous week and the current week are significantly higher in Abu Dhabi vs. Dubai primarily due to addressable market size. The pickup data suggests booking windows are currently extremely short with pickup variances, vs. previous years still showing good take-up.

Average occupancy levels for April 2026 stood at 34.5% for Dubai and 51.5% for Abu Dhabi.

As of 2 May 2026, occupancy levels have been steadily increasing with 7-day occupancy levels for Dubai standing at 42.2% and Abu Dhabi at 60.1%, up from 27.1% and 45.9% respectively from the 7-day occupancy on 2 April 2026.

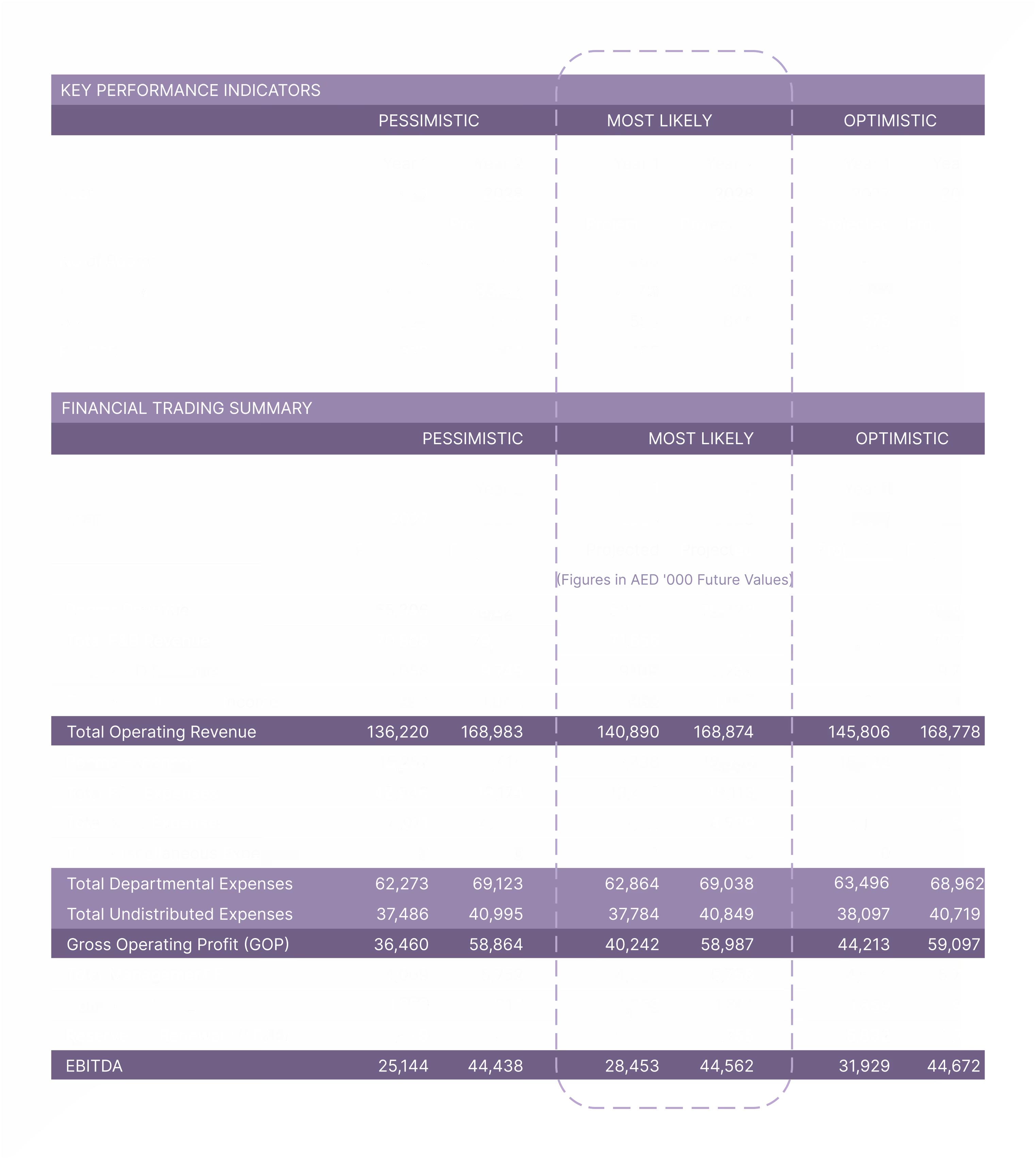

Scenario Analysis

Determining Impact

During periods of uncertainty, Real Estate X provides scenario analysis featuring an initial Base Scenario which is used to create a ‘most likely’, ‘optimistic’ and ‘pessimistic’ scenario to assist any reader make informed decisions.

Real estate is generally less susceptible to market volatility than equities or certain other financial instruments. However, it is subject to similar business challenges as overnight guest perception changes quickly during conflicts.

The hospitality market is responsive to demand changes and can adapt quicker than many other sectors, however it is also quickest to feel the effects of short‑term shifts in demand. This is because guest behaviour operates on very short booking cycles, often days or even hours. As a result, changes in sentiment, economic conditions, travel patterns, or external shocks translate almost immediately into occupancy and rate fluctuations.

The UAE has a healthy proportion of long-stay guests and sporadic staycation demand which supports occupancy levels at hotels. However, at the current occupancy levels demonstrated in the previous section, this base demand is insufficient to support a profitable asset. We analysed several assets performance during COVID to provide some working rationale on how hospitality assets had responded to the pandemic.

At certain daily rate levels, we saw hotels with mid 30% occupancy levels during 2020 still turn a profit. These assets were extremely fluid with their operational cost and managed to reduce department expenses by 30% and undistributed expenses by 24% despite a fall in total operating revenue of just over 45% for the year.

The COVID pandemic arguably provided more certainty than the current conflict, as hotels knew that the impact was going to be seen across the markets for a sustained period and could plan necessary action. Currently there is significant degree of uncertainty surrounding the conflict timescales and escalations; therefore, this creates a reluctance to make and plan operational changes.

In determining an opinion of impact, Real Estate X models three scenarios, in each scenario, year three of the forecast is assumed to mirror the base scenario. Recovery levels have been modelled specifically based on demand behaviour assuming that de-escalation continues and the conflict will not continue over a protracted timescale.

We have used source market data and given weighting to the exceptional Government response when forecasting different types of hotels recover in the UAE (business, leisure, groups).

Sub-market segments will fare differently as well as the positioning of the asset, as evidenced from the pandemic. Midscale assets are typically affected moreso than upscale and luxury products as a concertina affect puts additional pressure to reduce rates. Assets with diversified demand (government, healthcare, logistics, domestic corporate) may display comparatively resilient base occupancy.

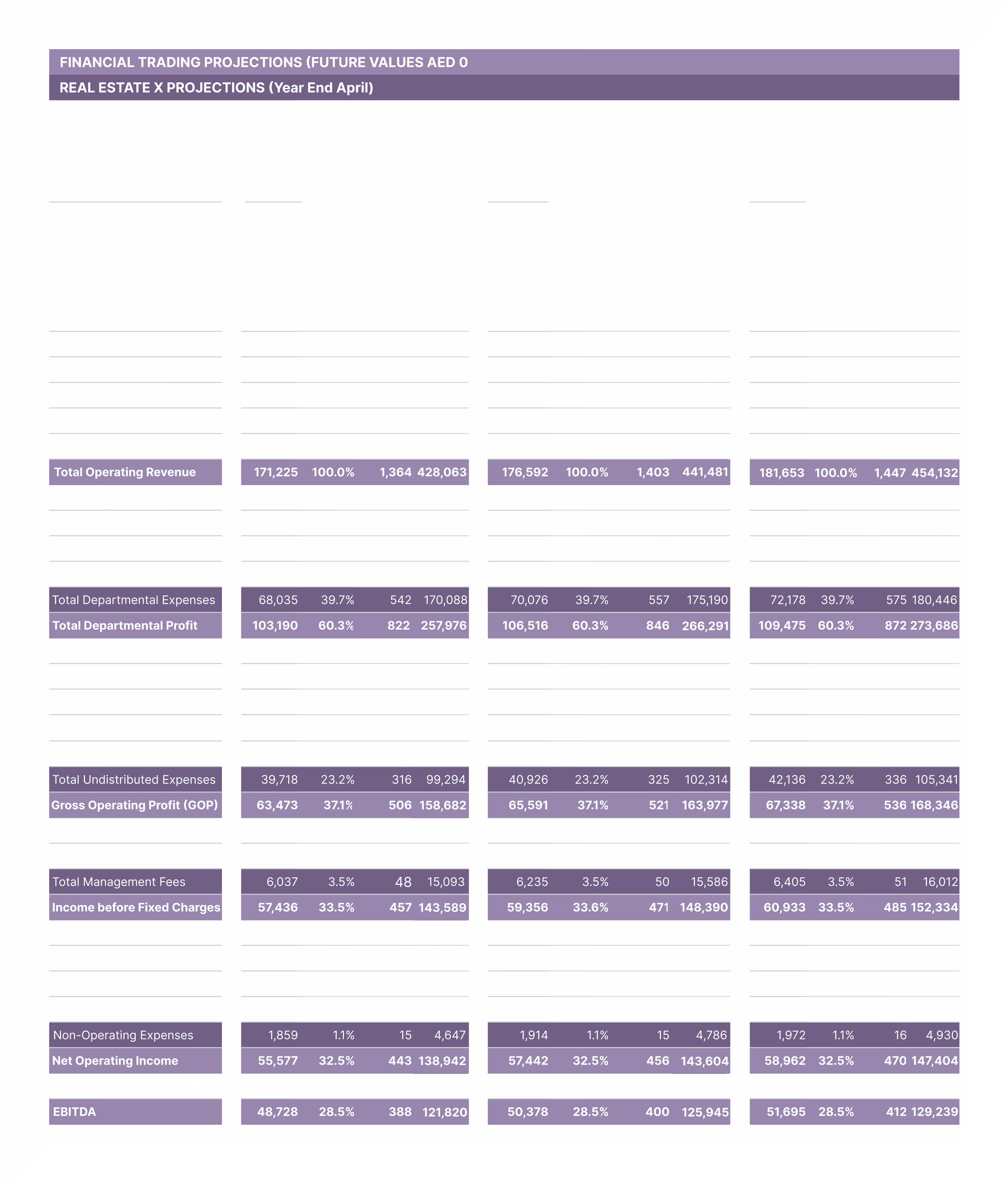

Base Scenario

Stage 1 - We replicate how we expected the asset to perform as of the valuation date, being 1 May 2026, assuming zero impact for the disruption caused by the instability. The example shown below mirrors an Abu Dhabi based, Luxury positioned asset, in close proximity to leisure demand drivers:

Forecast Adjustments

Stage 2, using the base scenario, we then apply required adjustments assuming de-escalation continues and the conflict will not continue over a protracted timescale.

Occupancy assessment:

- Using the pandemic performance as a benchmark, the hotels daily data suggests initial characteristics are similar, with a steep sharp fall in occupancy levels. Abu Dhabi achieved an average of 60.1% average occupancy during 2020. Assuming constructive negotiations continue, demand should return at a faster pace.

- Of the 5.9m hotel guests that Abu Dhabi saw during 2025, UAE Nationals have always made up the largest percentage, followed by the GCC and MENA markets, to return first due to short haul travel patterns. This should be closely followed by South Asia which is another one of Abu Dhabi’s biggest source markets, India standing at 13% of the total demand, having strong business ties and friends and relatives based in the region. CIS and Eastern Europe, we would also expect swift returns being historically resilient due to limited alternative warm-weather and visa-friendly destinations.

The below graph forecasts the most likely scenario, of demand recovery suggesting Abu Dhabi will end on a circa 70% average occupancy level for 2026. The graph is plotted against 2020 (covid) and 2025 occupancy levels with actual performance until 2 May 2026:

Further adjustments applied:

- ADR reduction evidenced by reduced demand and incentives. Based on sentiment surveys conducted during the pandemic and learning from demand behavior, an overwhelming majority of demand referenced security and safety as their primary concern, as opposed to attractive rates and incentives for travel.

- Per occupied room, food and beverage spend ratios typically increase due to the higher percentage of revenue coming from non-staying guests via walk ins and resident demand.

- Fixed cost structures to be shifted minimally in the interim, although the longer the regional conflict continues, the greater the need for adjustment.

Scenario Analysis

Scenario Results

The three scenarios provide the following percentage differences from Base Scenario:

20.4%

17.7%

14.8%

48.4%

41.6%

34.5%

4.2%

3.7%

3.2%

This analysis is cross checked against operational benchmark performance across Abu Dhabi during COVID where the differences between 2019 and 2020 full year performance was analysed. If expectations shift towards an elongated recovery, we expect hospitality assets to be able to further adjust cost profiles.

Sensitivity

Over 70% of the hospitality benchmarks analysed across the UAE generated a profit during 2020

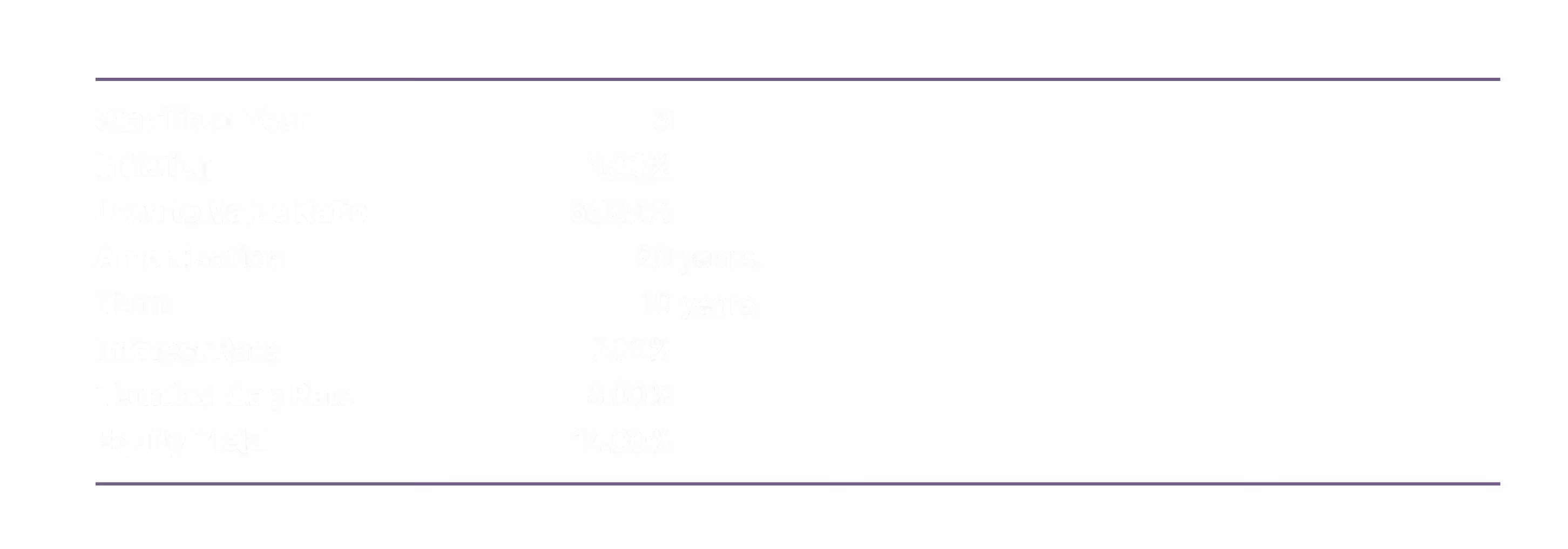

To assist the reader in understanding the dynamics of a discounted cashflow, Real Estate X uses a proof of value concept and a return analysis to justify any opinion of value.

For a proof of value concept, we convert the financial forecast into an estimate of value by applying market debt and equity ratios to confirm the results produced. The aim is to assess whether the determined cashflow can in turn satisfy a market lead financing structure and sustain mortgage and equity returns. In addition, the model will determine to what extent the forecasts provide a ‘supportable value’. In the Most Likely Scenario referenced, using the following assumptions provides for a supportable value of 99.9%:

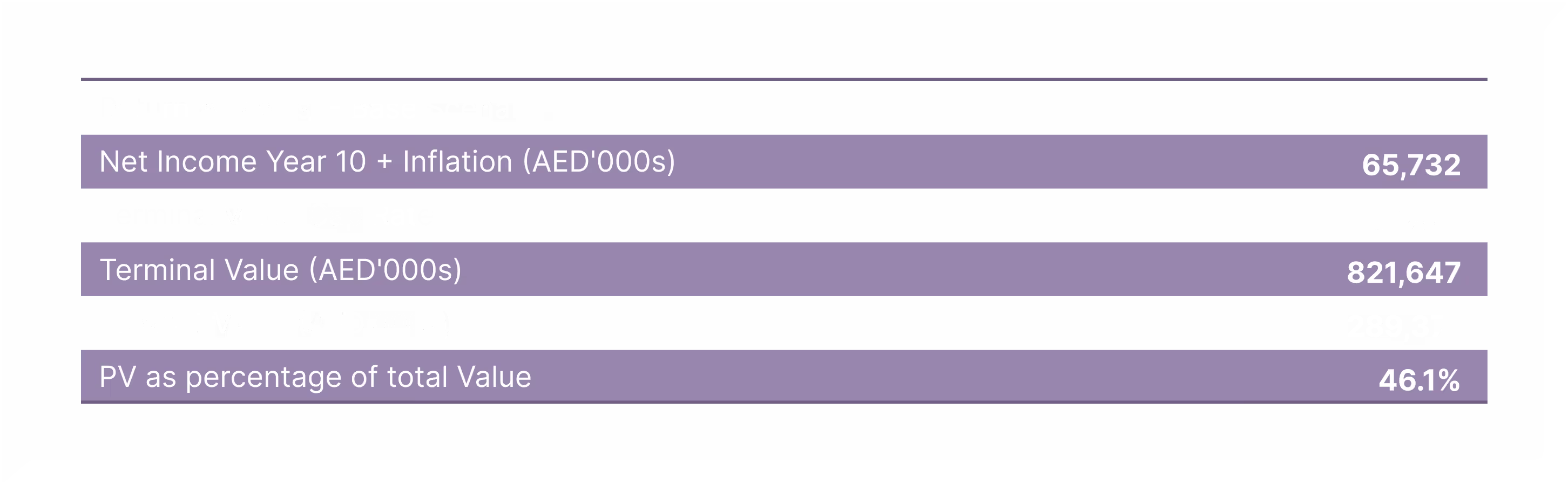

To take this a step further, from analysis of the forecasted cash flow, it is helpful to analyse the weighting of total value between the forecasted cash flow and the present value of the terminal value.

Using our Base Scenario, the present-day value of the terminal value is equal to 46.1% of the total value, this in-turn suggests 53.9% of the total value is attributed to the cashflow.

This 53.9% is split over the 10-year forecast and due to discounting Y1 provides for 13.7% of the total value attributed to the cashflow. In our Base Scenario example, this represents 7.37% of the total value, which suggest that if hotels were only able to break even during the first year of analysis, we would expect a circa 7.5% impact on value.

Summary

The Real Estate X team have valued assets through two market cycles, through political unrest, the Covid 19 pandemic and now the latest Gulf conflict.

Key Takeaways

- The source market, hotel type and positioning of the asset is key to determining recovery time, the biggest single source market for the UAE being India, which with short haul flights and easy reach will likely be quick to return. In fact, a significant proportion of UAE demand is either locally driven from the GCC or MENA regions.

- On-going transactional activity will likely continue as normal as evidenced by activity seen during the pandemic where agreed deals went ahead on similar terms.

- The UAE governments ongoing handling of the crisis and the UAE brand policy supports traveler perception and should mitigate a prolonged recovery.

- Whilst demand is returning as anticipated, proactive Banks can help maintain continuity, protect long-term asset value and distressed exits by providing flexible loan terms in the short term.

- Hospitality valuations are subject to multiple inputs with a heavy focus on future receivables. As a result, short term volatility in ADR and occupancy rates, even if material declines occur, do not have an overbearing impact on Market Values.

Explore Our Latest Insights

This blog explores the importance of surrounding yourself with like-minded individuals, mentors, and networks that can provide guidance, encouragement

.webp)